Bangladesh through a Chinese investor's lens.

A field briefing for capital looking out from China — mapping Bangladesh's politics, demographics, economy, and sector ecosystem against China's own development timeline. The thesis: Bangladesh today rhymes with China somewhere between 1995 and 2008, depending on the metric.

An updated edition. v2 adds the opening on Beijing and Dhaka, a chapter on why Bangladesh can compress China's twenty-five-year climb into roughly ten years, the climate stakes, the launch of the Zeph New Energy Fund, and the BSIC fund launch of 12 May 2026 as it happened.

Read the earlier version (v1) →China then, Bangladesh now.中国的当年,孟加拉的今天

I came to China 25 years ago. A kid with a dream to travel, write and take pictures. 25 years later, I landed in Dhaka, I'd become a startup operator and VC. And I felt... at home. That old China energy is in Dhaka today. It's time to invest. This is that story.

Two photo essays, twenty years apart set side by side they illustrate the rhyme. Beijing was once where Dhaka is now.

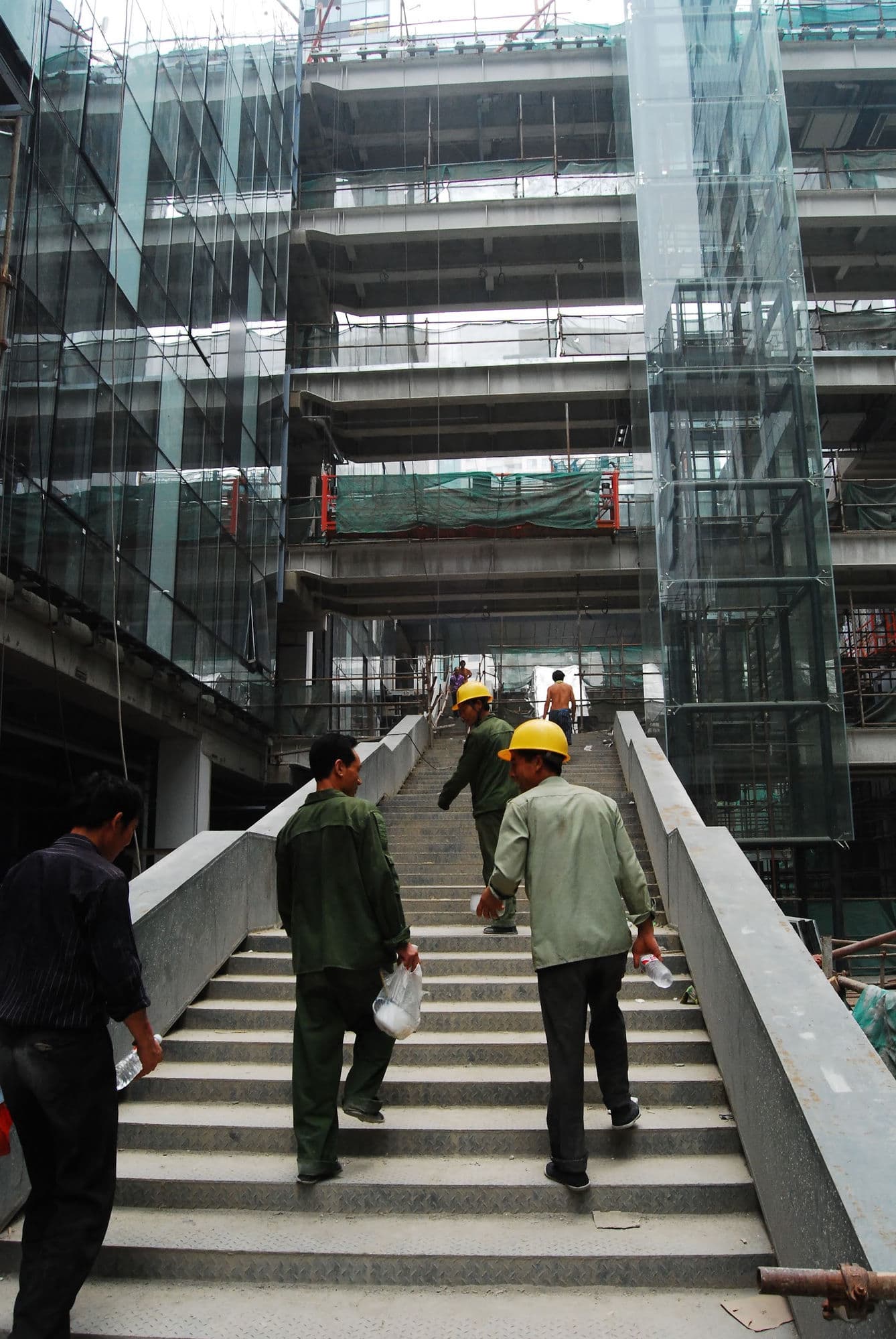

I landed in Beijing at the end of December 2000 — a nineteen-year-old kid, too young to drink alcohol in my own country. Two days later it was New Year's Eve, and a chance encounter landed me at an open-bar party in an expat apartment.

It was the kind of crowd you only get in a city that hasn't yet decided what it is: expat kids raised half-feral between countries, the privileged teenagers of diplomats — a clique of Uyghur and Kasakh intellectuals from Peking University in a corner, and the first children of China's elite, back from schools abroad in another.

The center of gravity was foreign. The Chinese future was in the room, but only as children. Nobody there had capital. China had not joined the WTO — that was still a year away. But the energy was palpable: everyone was up to something new, and making money at it. Someone offered me a job. I took it, and stayed thirteen years.

It's been twenty-five years. China grew up — and so did I.

My first day in Bangladesh — Independence Day, as it happened; the country was celebrating becoming a nation. This time there was no backpack. A startup founder met me at the airport; I had just dined with an exited founder, and a celebrated VC invited me to a party. It was déjà vu. History doesn't repeat itself, but it rhymes.

And the room had Beijing's old energy — but the guest list had moved on. Not the young and the foreign this time: one of the country's biggest venture capitalists. Development-bank officers. Garment-factory owners. Political operators who had outlasted a half-dozen governments. A yogi. Everyone was excited about a new government and the capital starting to flow, and a little nervous too: the Hormuz energy crisis, a warming world, a region in transition.

Beijing in 2000 had the energy of a country about to happen. Dhaka in 2026 has that same energy.

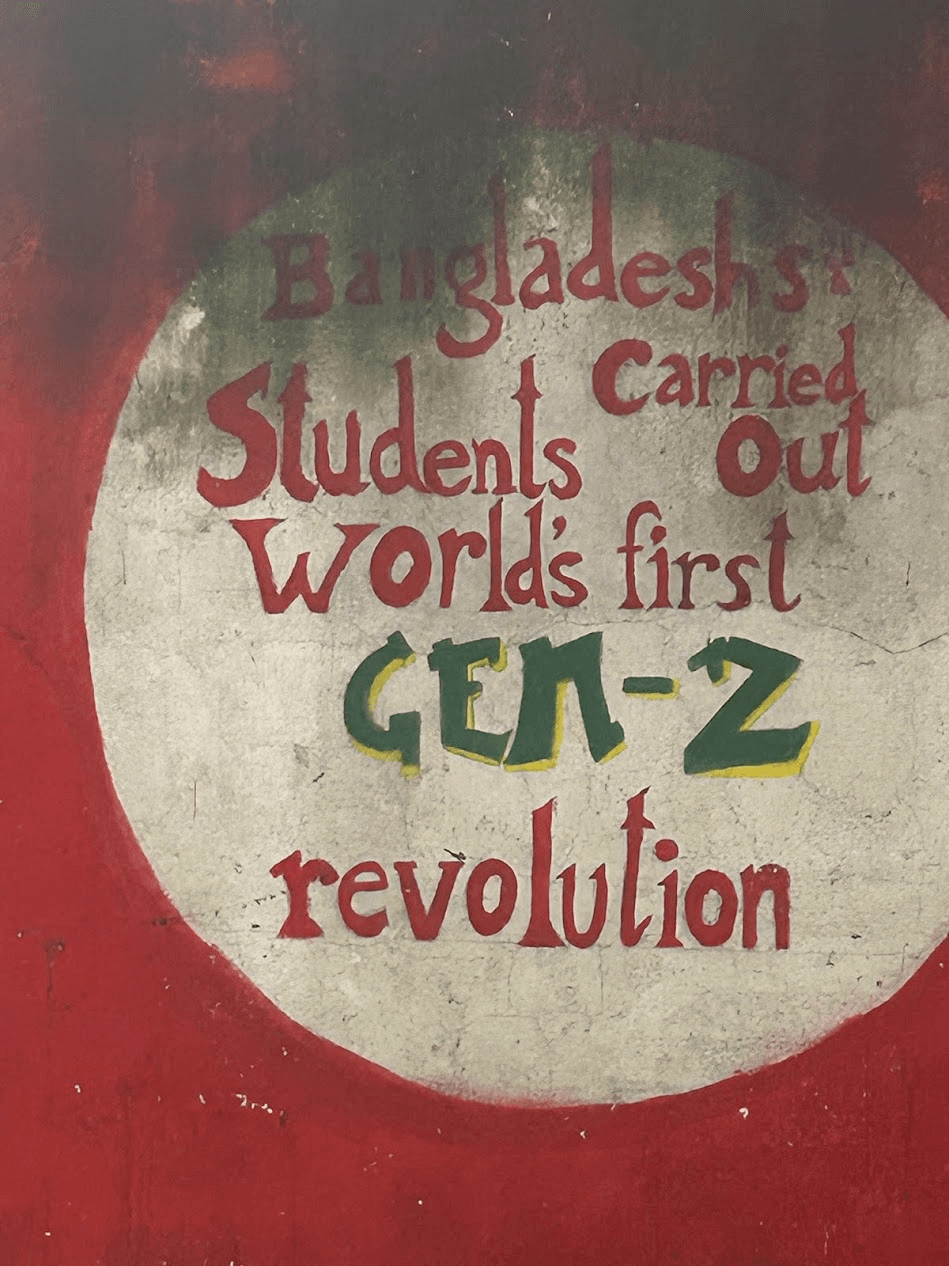

China grew up in the last 25 years. Bangladesh can do it in 5-10.

The top-10 country the world's been ignoring.被忽视的人口大国

Bangladesh is the 8th-most-populous country on earth. 175 million people — more than Russia, more than Japan, more than Germany and France combined. This is not a small, poor country tucked into the map of South Asia. It is a major nation with a new generation of hard-working youth revolutionaries, a new government, and a mandate for change.

Bangladesh holds more people than Guangdong — China's most populous province — on a land area almost exactly the size of Liaoning. A huge, dense, contained, fast-urbanizing market: short corridors, one connected grid of cities. For a transport company, density isn't the problem. It's the product.

The Zeph New Energy Fund is being assembled now. Join the list for field notes from Dhaka and the next edition of this report.

Bangladesh today ≈ China when?孟加拉的今天 = 中国的哪一年?

Bangladesh in 2026 sits roughly where China did between 1995 and 2008 — the exact year depends on the metric, and the chart below maps each one. Bureaucratic execution is, frankly, slower than China ever was; but English skills are better, politics are opening up, and AI is spreading fast.

To me, Dhaka today has that feeling that Beijing had post-WTO, pre-Olympics. Everything is possible. There is demand everywhere. You can walk into any room and make a deal. There's a group of people who are smart and hungry and educated and are going to succeed. It's quite a time to invest in Bangladesh.

A young country, with a 30-year demographic window.人口结构 · 仍处于人口红利窗口期

Bangladesh's median age is 27.6 — almost identical to China's in 1995, and twelve years younger than China's ~40 today. About 2 million workers enter the labor force every year. The dependency ratio is at its most favorable point for the next two decades.

For Chinese investors used to facing a contracting domestic labor force, Bangladesh offers a 20–30 year window of structural labor abundance. The labor cost arbitrage is durable — not a 5-year window like Vietnam.

$2,911 — exactly where China was in 2007.人均GDP · 相当于中国2007年水平

Bangladesh's nominal per capita GDP in 2026 is projected at $2,911, having just overtaken India ($2,812). For context, China crossed that threshold in 2007 — the year before the Beijing Olympics, just ahead of the post-2009 stimulus boom. Bangladesh's runway, if growth re-accelerates, is enormous.

What's behind the number

- Economy size · ~$510B nominal, ~$1.7T PPP — roughly the size of Vietnam.

- Growth · ~3.5% in FY24-25, projected to rebound to ~4.8% in FY25-26 (World Bank) — still below the 6–7% norm of the Hasina decade, but recovering on strong exports and record remittances. Banking stress and post-uprising disruption linger.

- BNP target: $1 trillion GDP by 2034 — i.e., roughly doubling in 8 years. Implies sustained 9% growth. Aggressive, contested by economists, but signals direction.

- Inflation · ~8.7% · stubborn, eroding real wages.

- FX reserves sit near $34B gross (≈$30B on the IMF measure, May 2026) and are recovering — but the 2026 Strait of Hormuz oil shock is a fresh strain. Brent spiked past $120 in March; Bangladesh, a heavy fuel importer, was among the region's hardest hit. It sharpens every argument here for electrification: each litre of imported diesel displaced by solar or an EV is foreign exchange saved.

40% urban — China's 2003 inflection.城市化 · 类似中国2003年节点

Bangladesh is ~40% urbanized. China crossed 40% in 2003 and proceeded to add ~25 percentage points of urbanization over the next two decades — fueling housing, infrastructure, durables, and service consumption at industrial scale. Bangladesh has the same migration wave still coming.

The honest read: weaker than China at every comparable stage — but English is the ace.教育与人力 · 整体落后中国当年,但英语是亮点

Tertiary enrollment is around China-2008 levels; the top universities sit near China-2000, the mid-tier well behind. The compensating advantage is English — materially better than China's at any comparable stage, unlocking the services and BPO export models China never fully captured. And AI shifts the picture again, lifting capability at every level faster than the universities can.

Universities to know

- BUET — Bangladesh University of Engineering & Technology. The "Tsinghua of Bangladesh." Engineering, software, infrastructure talent. Where investors should source senior technical hires.

- University of Dhaka. Oldest, most politically active. Strong in economics, policy, social science.

- North South University, BRAC University, IUB. Top private universities. Business, computer science, English-medium instruction.

- 28 Bangladeshi universities appeared in Times Higher Education Asia Rankings 2026. None in QS World top 400 in 2024.

University administration is politicized — appointments by loyalty, student politics disrupting semesters, curricula slow to integrate AI/cloud/coding skills. Firms hiring at scale should expect to interview many candidates per role and train fresh graduates from scratch, similar to China-2005 hiring practice.

650,000 freelancers and counting — a global services hub, not a product hub.科技人力 · 全球最大的自由职业者市场之一

Bangladesh is one of the world's largest freelancer markets — frequently ranked just behind India — with over 650,000 active and perhaps a million more informally connected. The ICT sector is ~$9.4B and growing 6%+ annually. But the model is closer to India-style services than China-style product. There is no Bangladeshi Tencent, Alibaba, or BYD analog.

Numbers worth remembering

- 4,500+ registered software/IT companies · 400,000+ employed professionals.

- ~1M freelancers earning ~$500–$700/month — 5x the entry-level corporate salary (~$100–$115/mo).

- $500M+ annual FX from freelance services — quietly significant for the trade balance.

- 5G rollout begins 2026, 4G is nationwide.

- Talent gap: senior AI / cloud / DevOps. Entry-level saturated; senior scarce. Wages for experienced engineers are ~$700–$1,500/month — under half of Vietnam, ~one-quarter of China.

- ~72% of households own a smartphone — up from 52% in 2022; 91% of adults use a mobile phone. The digital consumer market is not coming. It is already here.

Build offshore engineering centers, R&D back-office, and 24/7 customer support hubs. Partner with established Bangladeshi firms (Brain Station 23, Tiger IT, Vivasoft, Selise). Avoid trying to replicate WeChat-style super-app models — local consumer behavior runs through bKash + Daraz already.

The cost story: 23-year-old China prices, today.工资水平 · 相当于中国2003年

Garment sector minimum wage is $113/month. National average is ~$220/month. Mid-level engineers cost ~$700–$1,500. China's manufacturing wages were at this level in 2003. The cost arbitrage is real and durable, given the demographic structure.

Wage benchmarks · 2026

| Role | Bangladesh | Vietnam | China (today) |

|---|---|---|---|

| RMG / garment worker (entry) | $113/mo | $240/mo | $650/mo |

| Factory line supervisor | $300/mo | $600/mo | $1,200/mo |

| University fresh grad (corporate) | $250–$400/mo | $450–$700/mo | $1,400/mo |

| Mid-level software engineer | $700–$1,500/mo | $2,000–$3,500/mo | $4,000–$6,000/mo |

| Senior PM / dept head | $1,500–$3,000/mo | $3,500–$6,000/mo | $8,000–$15,000/mo |

One product carries 81% of exports. That is both the power and the problem.出口结构 · 服装一柱擎天

Bangladesh is the world's #2 garment exporter after China. RMG (ready-made garments) is 81.5% of all exports. The country has the most LEED-certified textile factories in the world (268, including 68 of the global top-100). But it also has one of the most concentrated export profiles of any major economy — diversification is a strategic imperative.

Why this matters for Chinese capital

- "China + 1" is real. Western brands are deliberately diversifying out of China. Bangladesh is one of three winners (Vietnam, India, Bangladesh).

- LDC graduation ends EU EBA tariff-free access — though the government has asked the UN to defer it three years, to 2029, buying time. Either way it pushes Bangladesh up the value chain into outerwear, technical wear, performance fabrics. This is the opportunity for Chinese fabric and machinery suppliers.

- Backward linkage gap. Knitwear is ~85% locally integrated. Woven (flat) fabric is only ~40%. Bangladesh imports billions of dollars of woven fabric from China — meaning a fabric mill investment in Bangladesh has a captive market.

- Adjacent sectors with room to run: pharma (export-capable, generics-heavy), leather, light engineering, ship-building/breaking, jute composites, frozen seafood.

Half the grid is already Chinese-built. The next wave is solar.能源电力 · 中国造发电厂占电网半壁江山

Chinese-built power plants supply 50%+ of Bangladesh's electricity. Going forward, Dhaka has set a 20% renewables-by-2030 target and 30% by 2040. Solar capacity is on track to grow from ~1.3 GW today to ~8.5 GW by 2035. This is one of the cleanest "Chinese capital wanted" stories in Asia.

I remember the exact moment everything changed, climate-wise, in China. It was September 2013, around 3:00pm — I was in a taxi on Guanghua Lu in Beijing. The taxi driver had the radio on. You have to understand: at that point Beijing was deep in an air-quality crisis. AQI hit 500 — the top of the US scale — for something like 200 days of the year. The scale literally ended at 500. **We called them yellow days.** For years the only public PM2.5 data anyone trusted came from the US Embassy's @BeijingAir feed. The radio announced Xi Jinping's State Council had released the "Action Plan for the Prevention and Control of Air Pollution" — committing every major city in China to publish PM2.5 and meet hard reduction targets. I jumped with joy and literally bumped my head on the ceiling of the taxi. *Everything's going to change.*

Live opportunities · 2026

- 523 MW solar PPAs signed January 2026. More tenders ongoing, including 77.6 MW in April 2026.

- Rooftop solar program targeting ~1,454 MW connected to grid by early 2026.

- ~760 MW/year of renewables needed Jan 2026 → Dec 2030 to hit the 20% target.

- Battery storage just emerging — almost zero installed today, mandated in newer tenders.

- Land scarcity is the real constraint — densely populated country, agricultural land politically protected. Floating solar, rooftop, and dual-use models are the path.

- Electrification is already running bottom-up — millions of battery rickshaws and 'easy-bikes' on the road, but almost no electric cars, trucks, or public charging. The government, reluctant to spend scarce foreign exchange on imported diesel, has every reason to push it further — and in May 2026 it did: the cabinet waived import duty on brand-new electric buses and trucks, cutting their total tax to roughly 15%, a window open through June.

- Capital is expensive — except green capital. Commercial lending runs 12–14%, a real brake on ordinary investment. Concessional green-financing windows sit near 4% — a structural subsidy quietly tilting new capacity toward solar, storage, and EVs.

Promised $40B, disbursed ~$7B, contracts $23B — the BRI math.中孟关系 · "一带一路"账本

The relationship was upgraded to a Comprehensive Strategic Cooperative Partnership in July 2024. BRI participation since 2016 has produced uneven results — large headlines, slower disbursement, but unmistakable infrastructure footprint. Under the new BNP government, both sides are negotiating an upgraded China–Bangladesh Investment Agreement.

Major Chinese-built / -funded projects

- Padma Multipurpose Bridge (rail link). Game-changer — connected southwest Bangladesh to Dhaka, cut transit times from a day to hours.

- Karnaphuli River Tunnel (Chittagong). First underwater road tunnel in South Asia.

- Payra Power Plant — 1,320 MW coal. Major baseload contributor.

- Multiple bridges, highways, rail — including 7 railway lines totaling ~600 km.

- Chinese Economic & Industrial Zone (Chittagong) — dedicated SEZ for Chinese manufacturers.

The BRI relationship has been more "China builds, Bangladesh pays" than equity FDI. Chinese contractors win construction work; loans come from China Exim Bank or CDB; equity ownership stays with Bangladeshi or government counterparts. This is now shifting — both sides have agreed to negotiate equity-based investment terms.

What unlocked China after 1980 — and where Bangladesh's equivalent unlocks are.瓶颈解除框架 · 借鉴中国1980-2000经验

This is exactly the right lens. Below is the equivalent map for Bangladesh — what bottlenecks exist, which ones the new BNP government is signaling it wants to clear, and which ones outside capital (Chinese in particular) can profit from clearing.

| Bottleneck | China 1980 state | China 1980→2000 unlock | Bangladesh 2026 state | Likely unlock path |

|---|---|---|---|---|

| Ownership / incentives | State-owned, no incentives | SOE reform, household responsibility, dual-track pricing | Heavy crony-cap; Hasina-era oligarchs being unwound | Anti-corruption push, contract review, opening sectors to private/foreign |

| Credit / debt | No personal/private debt | Banking system stood up, mortgages, business credit | Banking fragile, mortgage market tiny, private credit thin | Bank cleanup, deepen mortgage market, foreign banks expansion |

| Family/housing structure | Multi-gen households, work units | Nuclearization → demand for new homes, appliances, furniture | Still multi-gen common; rapid urbanization beginning to split | Affordable urban housing, white goods, motorbikes, 'bangla-teslas', e-commerce |

| Land use | Collective; rural-locked labor | Land-use reform; SEZs (Shenzhen 1980); rural→urban flow | Densely populated; SEZs exist but slow; land acquisition political | Faster SEZ expansion, dedicated industrial parks, dual-use solar |

| External capital openness | Closed | WTO entry 2001 → export manufacturing boom | Open in policy, slow in practice; LDC graduation Nov 2026 | Bilateral investment agreements (China-BD upgrade in negotiation), FTA push |

The five Bangladesh unlocks Chinese capital can profit from

- Banking modernization. Same playbook as 1998–2003 China — clean balance sheets, attract foreign banks, deepen consumer credit. Chinese fintech / bank tech vendors should be at the table.

- Affordable urban housing. 1.5M people/year flowing into cities, almost no formal mortgage market. Construction, materials, appliances — China's 2003–2010 winner playbook applies directly.

- Mass-market motorization. Two-wheelers and small EVs are about to take off — same pattern as China 2000–2008. BYD, Yadea, Niu, ride-hail platforms.

- Power infrastructure. 760 MW/year renewables required just to hit 2030 target. Chinese solar, BESS, transmission, EPC firms.

- Industrial supply chain depth. Bangladesh imports the components for its export champion sector. Fabric mills, dyeing, machinery, packaging, logistics — high-margin gaps Chinese firms can fill.

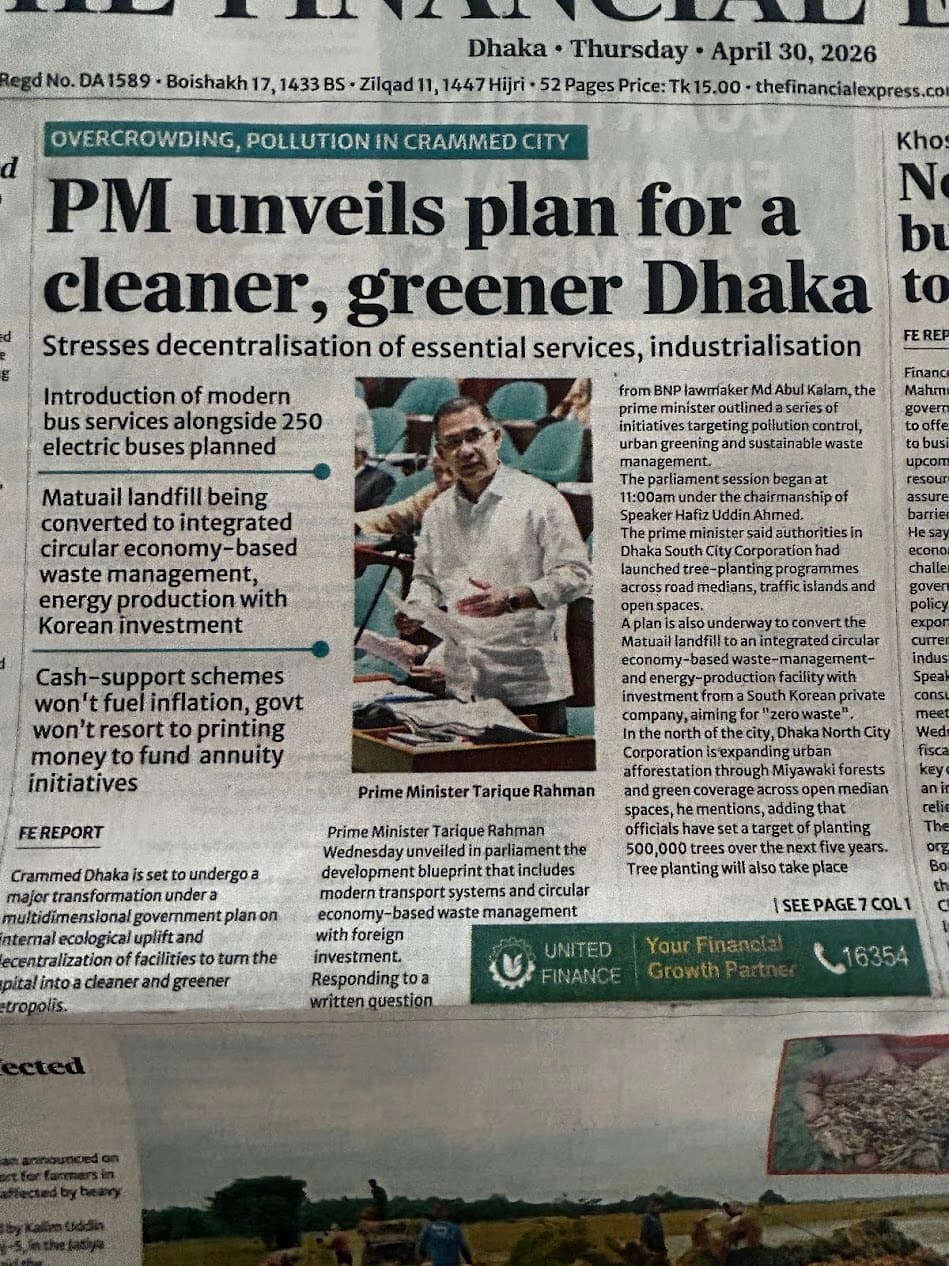

The new regime: signals, moves, and what's already changed.新政府执政头78天 · 信号与动作

Tarique Rahman (BNP) was sworn in as Prime Minister on 17 February 2026. This section is current to 5 May 2026 — Day 78 — with later developments carried in the postscript. The early signals matter more than any single policy: this government is signaling continuity on FDI, an opening toward China, distance from India, and a domestic reform agenda. Here is what has actually happened, with dates.

What the first 78 days tell us about the next 5 years

- Pro-China tilt is real and structural. Two China visits in three weeks, public language warmer than the Hasina era ever was. China responding with concrete trade concessions.

- India relationship is cooler. India still hosts Hasina; that's a sustained sore point. Bangladesh is repositioning, not breaking — but the relative space for Chinese capital is wider than at any point in the past 15 years.

- Reform agenda is real but bureaucratically slow. The 180-day plan is concrete but modest in ambition. Anti-corruption and banking cleanup are flagged but execution will take years.

- Long-term targets are aspirational. $1T GDP by 2034 and 5x health spending are political signals, not credible plans yet. Still useful as direction-of-travel indicators.

- LDC graduation — the cliff the government is moving. Dhaka has formally asked the UN to defer graduation three years, to 2029, while racing to lock in alternative tariff arrangements; China's 99% tariff-free extension is the biggest single win so far.

- Clean energy is the clearest demand signal. The government targets 10,000 MW of renewables by 2030 — roughly 20% of the mix, about $9B of investment. But scrapping the sovereign-backed Implementation Agreements left a payment-security gap that has stalled new projects. That gap — bankable structure, not appetite — is exactly what disciplined outside capital can close.

- Political stability looks decent for now. Two-thirds majority means the government can move legislation; opposition is fragmented (Awami League weakened, AL leadership in exile).

If you've been waiting for a window — this is it. The new government is actively courting Chinese capital, has eased BRI loan terms in negotiation, and is signaling investment-agreement upgrades. The next 12 months will see a flurry of concrete projects announced. Position teams now.

Where to deploy capital · ranked.行业机会图谱

Heat-mapped against three things: (1) demonstrated demand, (2) China-side competitive advantage, (3) BNP government priority. Top-row sectors are where Chinese investors should be most aggressive in 2026–2027.

Solar EPC & modules HOT · 9/10

523 MW PPAs already signed in Jan 2026; ~760 MW/year needed to 2030. China dominates global solar manufacturing and EPC. Direct fit.

Battery energy storage HOT · 8/10

Mandated in newer renewable tenders. Almost zero installed today. CATL, BYD, EVE all relevant.

Fabric mills (woven) HOT · 9/10

Bangladesh imports billions in woven fabric, mostly from China. Local mill = captive market + LDC graduation cushion.

Two-wheel EVs & e-rickshaws HOT · 8/10

Replicates China-2005 motorbike inflection. Yadea, Niu, BYD bikes already entering. E-rickshaw fleet conversion is huge addressable.

Garment machinery & automation WARM · 7/10

As Bangladesh moves to outerwear / technical wear, demand for advanced cutting, stitching, finishing equipment grows. CN suppliers cost-advantaged vs. Japanese/European.

Construction & infra EPC WARM · 7/10

Already a strong segment. Watch for contract reviews — but pipeline is growing under BNP. Bridges, ports, urban transit.

Pharma manufacturing & APIs WARM · 7/10

BD pharma exports growing. CN API supply is the global default. Joint ventures attractive given local industry maturity.

White goods & appliances WARM · 7/10

Walton (local champion) covers basics; mid-premium gap exists. Haier, Midea, TCL all relevant. Local assembly preferred.

ICT / BPO offshoring centers WARM · 6/10

Offshore engineering, R&D back-office, customer support hubs. English fluency tilts this away from CN domestic alternative for Western-facing services.

Consumer e-commerce COOL · 5/10

Alibaba's Daraz is already the platform. Better as marketplace seller than as platform challenger.

Mobile money / fintech COOL · 4/10

bKash is entrenched and beloved. Hard to dislodge; better to partner.

Auto (passenger cars) COOL · 4/10

$2,911 per capita is below the auto-takeoff threshold (~$5,000). Watch, don't deploy yet — except for premium EV early-adopter tier.

What could go wrong.主要风险

Political volatility

- Two regime transitions in 18 months. Stability is recent, not proven.

- BNP-Jamaat coalition tensions could fracture the majority.

- Awami League supporters disenfranchised, potential unrest.

- Military remains the implicit backstop — historically intervened.

Macro / FX

- Inflation 8.7%, sticky.

- FX reserves stabilizing but recently strained.

- USD repatriation has had delays — improving but check current state.

- Banking NPLs not yet cleaned up; structural fragility remains.

Execution / bureaucracy

- Land acquisition slow, politically sensitive.

- BIDA improving but not Vietnam-grade.

- Power and gas reliability still factor in siting.

- Customs and ports congested (Chittagong).

Geopolitical & trade

- LDC graduation Nov 2026 ends EU EBA preferences.

- India relationship cool — overland logistics complicated.

- US tariff pressure on Chinese-linked production possible.

- Climate vulnerability — flooding, cyclones, sea-level rise.

Contract review risk

- BNP government auditing Hasina-era big-ticket deals.

- Some Chinese projects flagged as overpriced may face renegotiation.

- New deals more transparent but slower to close.

Talent depth

- Top-tier engineering talent thin (BUET only).

- Mid-skill manufacturing depth shallow outside RMG.

- Senior management bench limited; expat support often needed early.

Twenty-five years, in ten.二十五年的路,十年走完

When I first landed, Beijing ran on the Xiali — a tinny 1.2-litre hatchback, the universal red taxi of the era. This spring the same streets moved in the Voyah: a silent, electric, premium MPV that did not exist as a category five years ago. Combustion to electric, cheap to premium — that is the distance China crossed, and it took twenty-five years.

Everything in this report so far has been a diagnosis: Bangladesh in 2026 sits where China sat between 1995 and 2008. If that were the whole story, it would be an argument for patience — buy in, wait twenty-five years, collect the trajectory. It is not the whole story. Bangladesh will not need twenty-five years to cross that distance. It will need five to ten. Three things changed between China's climb and Bangladesh's.

1 — The toolkit is for sale now.

When China industrialized, it had to build the capacity to industrialize — the machine-tool industry, the solar supply chain, the battery plants, the EV lines, invented or painstakingly localized over decades, and badly at first. Bangladesh does not. The entire capital-goods catalog now ships, containerized, from a port three days away — the same robots, the same panels, the same cells a Chinese factory runs, at China's scale-cost. China climbed the ladder. Bangladesh takes the elevator — and it was China that built the elevator. I watched it get built: at Renren — China's Facebook — we copied the HTML and CSS straight off Facebook's pages, because in 2009 the technology was not for sale; you copied it or you did without. Today China sells it. The only thing now between Bangladesh and the catalog is Bangladesh's own import tariffs — and those, at last, are coming down.

2 — AI is the multiplier China never had.

China's twenty-five years were also twenty-five years of accumulating human capital — engineers, managers, the tacit knowledge of how to run a modern firm. That accumulation was slow because it happened one career at a time. Bangladesh is building its industrial base in the first era where a junior engineer or a first-time factory manager can borrow expertise on demand. AI does not replace the workforce. It compresses the learning curve — and the learning curve was most of the twenty-five years.

3 — Clean is now the cheap path.

China industrialized filthy — in 1995 it had no choice; coal was cheap, solar was a science project. It is still paying to retrofit. Bangladesh leapfrogs that, the way the developing world leapfrogged the landline. Solar is now the cheapest power ever built; an electric vehicle is cheaper to own than a diesel one. For the first time the cheap path and the clean path are one — and it was China that made the clean one cheap.

This is not a claim that Bangladesh replays all of China. What compresses is the industrial-capacity build — because that input went from something a country must invent to something it can buy. What does not compress is execution: the bureaucracy, the permits, the courts, the ports. The Bottleneck Framework and Risks sections of this report are not contradicted here — they are its other half. The machines arrive in ten years. Whether Bangladesh lets them off the dock is the open question.

I went back to Beijing this spring. My friends from the Renren days, when we were all young and pushing for an IPO, they made it! Most of them more than once. They ride in cars that drive themselves now, or have someone else drive their Maybachs. That is what twenty-five years bought them. Bangladesh can do it in five, or ten.

The world my children inherit.我的孩子将继承的世界

When I landed in Beijing at the end of 2000, the world was roughly one degree cooler than it is today — and we are starting to feel the difference.

In twenty-five years, when my children are the age I was at that New Year's Eve party, the world will be hotter still — and we are not on a path that stops at a number anyone finds comfortable. Two degrees is the optimistic case now. Three is the scenario we are all a little too afraid to think about — and the one this work exists to bend away from.

And Bangladesh is where that question gets answered first. A hundred and seventy-five million people; much of the country a metre or two above a rising sea; the largest delta on earth. Bangladesh does not get to industrialize the slow, dirty way and clean up later — the water arrives before the apology does. It has to build clean the first time. Which, as the last chapter showed, is now also the cheap way to build. The arithmetic and the necessity finally point the same direction.

That is why I am no longer content to only write about this.

Why I'm doing this.我为什么亲自下场

A fair question before I make the case: why take any of this from me?

I came to China in 2000 with a backpack. The early years were odd jobs — travel writing and photography for National Geographic Traveler, Fodor's, Harper's; packaging design; translation; five years teaching English, learning a word of Chinese for every word I taught.

Then I walked into another party and took a job at Xiaonei.com, which became Renren.com — "China's Facebook." We were running Google ads when Google was banned in China, and my job was to build the ad platform and sales kit "with Chinese characteristics."

In three years annual revenue went from $5M to $50M, and we IPO'd on the NYSE. A hundred and eighty days later I took my exit and turned up in Silicon Valley, at 500 Startups. That closed out thirteen years in China.

The decade since — back in Asia — has been venture capital and operating seats: Chief-Something-Officer at startups, then accelerator VC. I led teams that run in Mandarin, Bahasa, Singlish; read three thousand accelerator program applications; interviewed five hundred founders; voted on a couple hundred deals. Running Accelerating Asia's program I mentored fifty-six startups — every one raised a follow-on round, and nearly a quarter were Bangladeshi. I have backed eleven companies myself, and run a syndicate, Particle Alliance, that has done five deals more.

Then, in May 2025, I took a year off — learning to code for the fifth time in my life (the first was at twelve), this time with AI — turning over one question I could not put down: what if this is for more than selling more product? What if it is for saving the world? And then I went to Bangladesh.

That is why I am starting the Zeph New Energy Fund — to put capital, and my own time, into the clean industrialization of Bangladesh: the solar, the storage, the electric vehicles, and the factories that build them. Not as charity, and not as a bet on a distant future — as the most legible opportunity I have seen since the room I walked into in Beijing in 2000. Except this time I am not nineteen, and I am not just a guest at the party. What follows is the same case stated the way an investment committee would want it — flat, numeric, unsentimental; both versions are true.

The case in five lines

- 175M people · $2,911 per capita · median age 27.6. Demographically and economically equivalent to China between 1995 and 2008, depending on the metric.

- The new BNP government (Day 78) is tilting toward China. Two delegation visits in three weeks, eased BRI loan terms, 99% tariff-free access extended to 2028.

- Five priority sectors: solar EPC + BESS, fabric mills, two-wheel EVs, garment machinery, construction EPC. Each a direct China-supply-chain extension.

- Window: the next 24 months. Even with LDC graduation likely deferred to 2029, the contract-review wave and incumbent positioning close the early-mover gap fast.

- Risk-adjusted, this is one of the few remaining structural plays with China-2005-style upside in a relatively friendly regulatory posture.

The frame is already shifting.格局已经开始转变

I finished the first version of this report at the start of May. Nine days later I was in Dhaka again — in a ballroom this time, watching a venture capitalist launch a fund.

It is called BSIC, the Bangladesh Startup Investment Company. I did not need to read its pitch deck closely; it was on the screens behind the stage, in language I could have lifted from this report: The Structural Moment. Why This. Why Now. Bangladesh is not an emerging market — it is an arrived one. Capital for the next generation.

Two documents agreeing is not evidence — a coincidence until it is a pattern. But the frame here is not mine alone: an independent, entirely Bangladeshi institution looked at the same country, reached the same conclusion, and put real money behind it. And BSIC is no boutique — it is backed by thirty-nine banks, each pledging one percent of future profits, a structure built to channel a large, recurring flow of domestic capital into exactly this build. When separate people converge on the same read, that is signal.

The capital is already forming. The only question this report can leave you with is whether you are early, or whether you are late.

If any of this rhymed with something you have seen before, get on the list. Field notes from the ground in Bangladesh, the Fund's progress, and the next edition of this report — sent as it happens.